Self-Rental Agreement: What It Is and Why It Matters for Landlords and Tenants

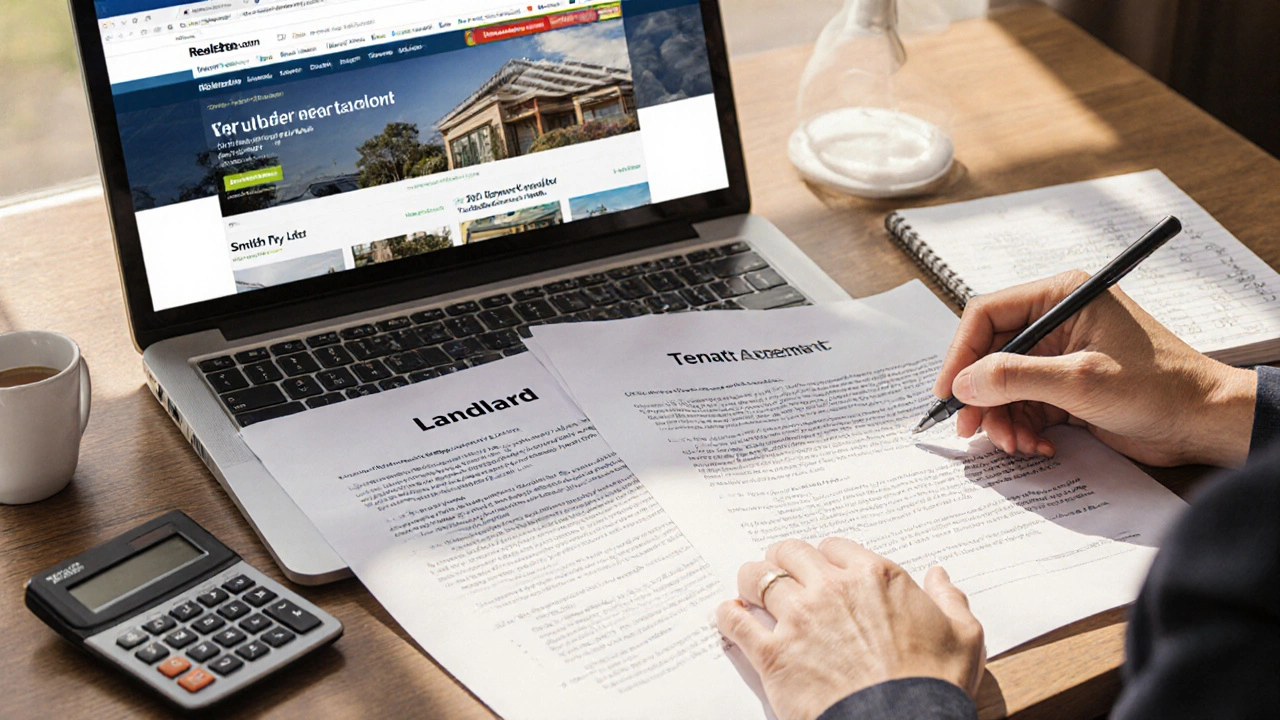

When you rent a property you own to yourself — say, through a business entity or a family member acting as the landlord — that’s called a self-rental agreement, a legal arrangement where the owner of a property enters into a rental contract with another party they control. Also known as self-rental arrangement, it’s not as weird as it sounds. People do it to separate personal and business expenses, manage tax liability, or handle family property transfers. But if done wrong, it can trigger audits, disallowed deductions, or even legal trouble.

A self-rental agreement, a legal arrangement where the owner of a property enters into a rental contract with another party they control. Also known as self-rental arrangement, it’s not as weird as it sounds. People do it to separate personal and business expenses, manage tax liability, or handle family property transfers. But if done wrong, it can trigger audits, disallowed deductions, or even legal trouble. isn’t just a handwritten note on a napkin. For it to hold up, it needs the same structure as any other lease: clear rent amount, payment schedule, duration, maintenance rules, and signatures. The IRS and courts don’t care if you’re renting to your LLC or your sibling — they care if the deal looks real. That means rent must match market rates. If you charge $500 a month for a property that others rent for $1,800, you’re asking for trouble. And if you skip a written agreement altogether, you lose legal protection on both sides. A handwritten lease, a legally binding rental contract written by hand, often used in informal or personal arrangements. Also known as handwritten rental agreement, it can be valid if it includes all key terms and is signed by both parties is perfectly legal — as long as it’s complete. But typed, signed, and dated documents are far easier to enforce.

Why do people even bother with a self-rental agreement? Often, it’s about taxes. If you run a business from a property you own, paying rent to yourself (through a company) lets you deduct that rent as a business expense. But the IRS has rules: the property must be used primarily for business, and the rental income must be reported on your personal return. You can’t dodge taxes by moving money from one pocket to another. Some use this setup for estate planning — transferring property to a child while still living there, with a formal lease to avoid gift tax issues. Others use it to protect assets, keeping personal and business finances separate. But every time you do this, you’re creating a paper trail. That’s good if you’re clean. Bad if you’re cutting corners.

What you’ll find in the posts below isn’t theory. It’s real-world guidance on what works — and what gets you sued. You’ll see how to write a binding rental agreement that holds up in court, what documents you actually need to rent your own property, and how to avoid the traps that catch most people doing self-rentals. There are also examples of how landlords in Maryland, Virginia, and Australia handle similar setups, and what happens when the agreement is vague or missing. No fluff. No jargon. Just what you need to know before you sign anything — whether it’s on paper, on a phone, or in your own handwriting.

How to Make a Legally Sound Rent Agreement with Yourself for Property Management

Learn how to create a legal rent agreement with yourself to claim tax deductions for home office use. Understand market rent rules, what you can claim, and common mistakes to avoid in Australia.